The global filter bag market is primarily driven by increasingly stringent environmental regulations, industrial expansion, and the rising need for efficient dust and particulate control across sectors. A filter bag is a critical component used in baghouse dust collectors to capture fine particulate matter from gas streams or liquid flows, ensuring compliance with air emission and process quality standards. According to the International Energy Agency (IEA), the industrial sector accounts for nearly one-quarter of global carbon dioxide (CO₂) emissions, highlighting the importance of advanced filtration systems, such as filter bags, in achieving cleaner operations and sustainability goals.

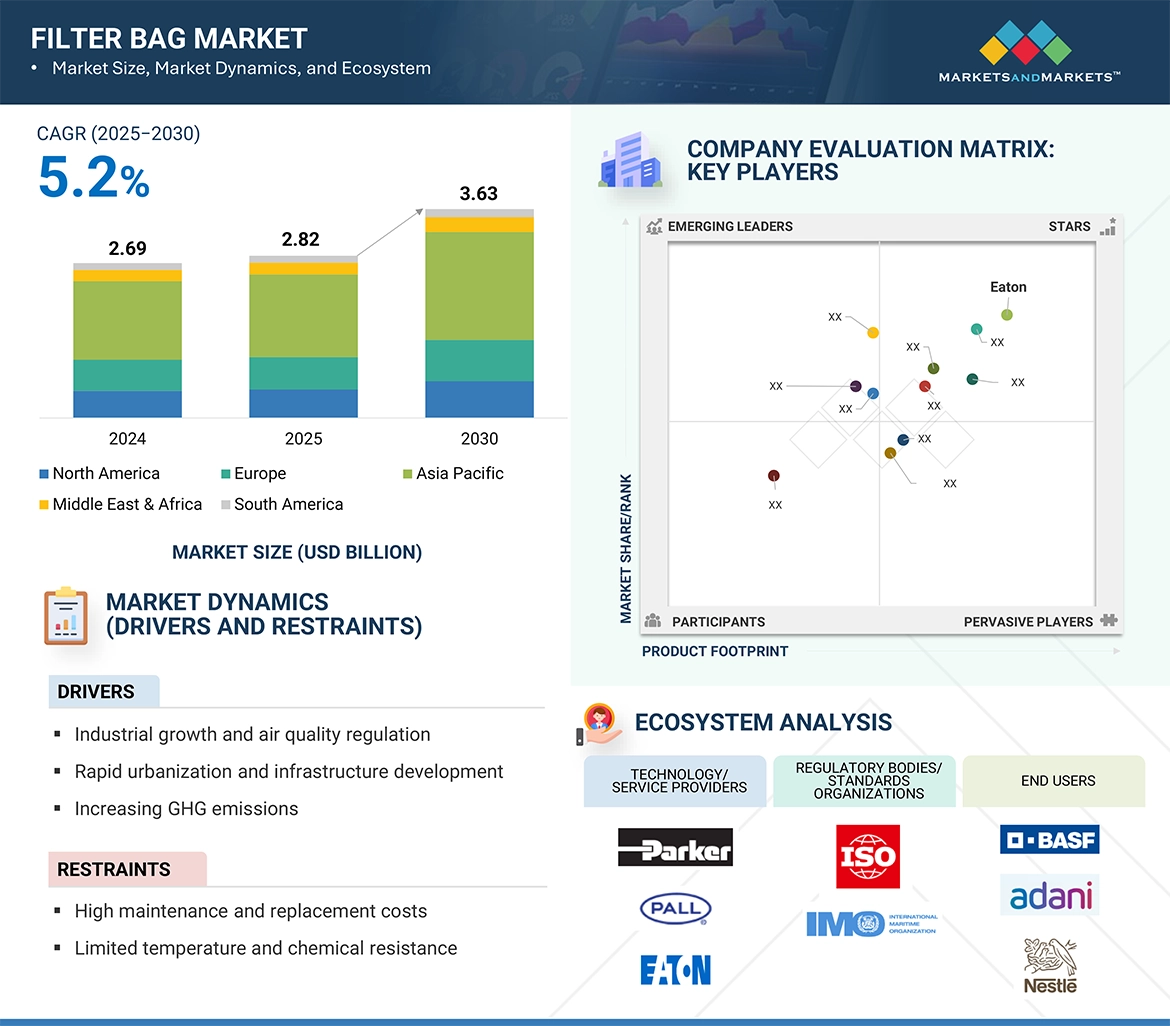

The global filter bag market is projected to reach USD 3.63 billion by 2030 from an estimated USD 2.82 billion in 2025, registering a CAGR of 5.2% during the forecast period.

Filter bags assist in solving present and upcoming challenges faced by industries, such as stricter emission norms, productivity pressures, energy efficiency requirements, and operational cost limitations. According to the World Cement Association, cement production alone accounts for nearly 7–8% of global CO₂ emissions, making high-performance filter bags indispensable in this and other heavy industries. While industries in North America and Europe are leading in terms of early adoption due to stringent environmental frameworks, Asia Pacific is witnessing rapid growth, driven by large-scale industrialization and government-backed pollution control mandates.

Download PDF Brochure – https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=139502740

A significant technological advancement reshaping the filter bag market is the development of advanced polymer-based and nanofiber filter media. These next-generation materials enhance dust capture efficiency, extend bag life, and reduce energy consumption in industrial operations. On the regulatory front, stricter emission norms such as the European Union’s Industrial Emissions Directive (IED) and the US Environmental Protection Agency’s (EPA) Clean Air Act push industries to adopt high-performance filtration systems. Furthermore, many Asia Pacific countries, including China and India, are introducing tighter pollution control measures and mandating cleaner industrial practices. These advancements and regulatory changes drive a shift toward innovative, durable, and energy-efficient filter bag solutions, fundamentally transforming the global business landscape.

The Asia Pacific filter bag market is estimated to be the largest and fastest-growing market during the forecast period. This region is also a global hub for manufacturing activities. China dominated the Asia Pacific filter bag market. The region is experiencing rapid development fueled by the growth of major economies, such as China, India, Japan, and Australia. Japan is investing in advanced, sustainable filtration technologies to comply with carbon neutrality goals. Southeast Asian nations are emerging as new growth hotspots due to booming construction, mining, and industrial sectors. Additionally, regional governments are tightening air quality standards and pushing industries to adopt eco-friendly solutions, creating significant opportunities for high-performance and technologically advanced filter bags.

The gas filtration segment dominates the filter bag market, depending on the filtration type. It is extensively deployed in various industries, such as cement, power generation, steel, and chemicals, where controlling emissions and dust from flue gases is critical. The increasing demand for high-temperature-resistant fabrics, such as fiberglass, aramid, and polyimide, in gas filtration is driven by stringent global emission standards (the US EPA Clean Air Act and the EU Industrial Emissions Directive). On the other hand, liquid filtration is becoming increasingly important across industries such as food & beverage, pharmaceuticals, oil & gas, and chemicals, where product purity and process safety are essential.

The filter bag market for the non-woven media segment dominates due to its higher dust-holding capacity, energy efficiency, and longer service life, making it the preferred choice across heavy industries such as cement and power. Non-woven media also offer better resistance to high temperatures, chemical exposure, and abrasive particles, enhancing operational reliability in demanding industrial environments. With advancements in polymer technology and the integration of nanofiber layers, non-woven filter bags now provide superior filtration efficiency while minimizing pressure drop, thereby reducing overall energy consumption. Growing emphasis on sustainable manufacturing has further accelerated the adoption of non-woven media, as these bags are increasingly designed for recyclability and lower environmental impact.

Make an Inquiry – https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=139502740

The filter bag market presents significant opportunities driven by rising global demand for cleaner industrial operations, stricter emission control regulations, and rapid industrial expansion in emerging economies. Key growth avenues include the increasing adoption of advanced filtration systems in cement, power generation, mining, and chemical industries, and the shift toward energy-efficient and eco-friendly solutions. Growing investments in infrastructure development, particularly in Asia Pacific, further fuel the demand for high-performance filter bags. Key players can tap into these opportunities by focusing on innovation in high-temperature-resistant and nanofiber-based filter media, offering customizable solutions for industry-specific needs, and expanding their presence in fast-growing markets through strategic partnerships and localized manufacturing. Developing sustainable and recyclable filter bag solutions will also align with global decarbonization and circular economy goals, strengthening long-term competitiveness.