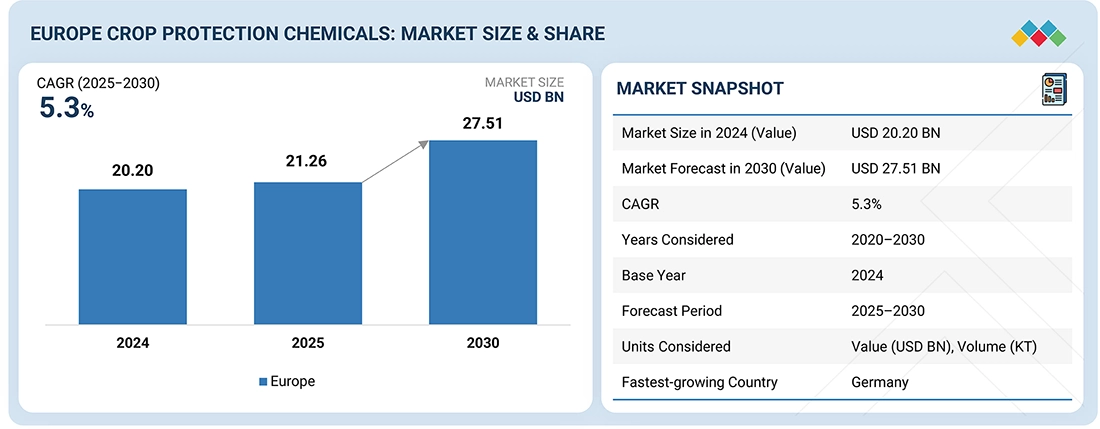

This Europe Crop Protection Chemicals Market Overview highlights a sector on a steady growth trajectory, projected to expand from USD 21.26 billion in 2025 to USD 27.51 billion by 2030, registering a CAGR of 5.3% during the forecast period. This growth reflects a convergence of technological innovation, rising demand for high-quality agricultural output, and the urgent need for sustainable farming systems across the region.

Europe’s agricultural sector is undergoing structural transformation, driven by digitalization, precision agriculture, and the transition toward environmentally responsible crop protection solutions. Integrated pest management (IPM) programs, bio-based formulations, and microbial solutions are increasingly aligned with the European Union Green Deal, reinforcing the shift toward sustainable crop productivity and reduced chemical dependency. These developments are reshaping the Europe Crop Protection Chemicals Industry, positioning it as a model for sustainable agri-input transformation.

Growing government support for agricultural modernization, rising adoption of liquid formulations, and increasing investment in research and development of residue-free and eco-friendly products are creating new innovation pathways across Europe’s crop protection ecosystem. These developments are reshaping competitiveness and redefining long-term market dynamics.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=190542011

Herbicides Segment Dominates the Market

Herbicides account for the largest share in the type segment of the Europe crop protection chemicals market. Their dominance is primarily driven by their critical role in weed control across major crops such as cereals, oilseeds, and pulses.

Weeds compete aggressively with crops for nutrients, water, and sunlight, leading to significant yield losses if not effectively managed. As a result, herbicides remain essential inputs in both conventional and conservation tillage systems across European farms.

Market expansion in this segment is supported by:

- Continuous innovation in selective and broad-spectrum herbicides

- Development of low-dose combination formulations

- Adoption of precision agriculture technologies

- Integration of integrated weed management (IWM) systems

Advanced formulations now deliver higher efficacy with reduced environmental load, aligning with Europe’s sustainability mandates. Reliability, performance consistency, and compatibility with modern application technologies continue to secure herbicides as the backbone of commercial farming operations across the region.

Soil Treatment: A High-Growth Application Segment

The soil treatment segment is expected to hold a significant share among modes of application during the forecast period. Soil treatment plays a vital role in:

- Improving soil health

- Preventing pest infestation

- Enhancing nutrient availability

- Supporting long-term crop productivity

European farmers increasingly rely on soil-applied fungicides, insecticides, fumigants, and bio-based solutions to address soil-borne diseases, nematodes, and root health challenges—particularly in high-value crop production such as fruits, vegetables, and cereals.

Key growth drivers include:

- Integrated soil management practices

- Bio-based soil treatment solutions

- Controlled-release formulations

- Precision agriculture integration

As sustainability becomes central to European agricultural policy, soil treatment technologies are emerging as a core pillar of environmentally responsible farming systems.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=190542011

Germany: A Strategic Hub for Crop Protection Innovation

Among European countries, Germany is estimated to hold a significant share of the crop protection chemicals market. The country’s leadership is supported by:

- Large cultivation areas for cereals, oilseeds, and sugar beets

- Strong regulatory compliance culture

- Advanced adoption of IPM systems

- High penetration of digital farming technologies

- Rapid uptake of bio-based formulations

Germany’s agricultural ecosystem benefits from robust R&D infrastructure, strong public–private partnerships, and continuous investment in sustainable crop protection technologies. The presence of major global agrochemical players further strengthens its position as a regional innovation and commercialization hub.

With increasing focus on environmental protection, ecosystem balance, and productivity optimization, Germany continues to act as a strategic growth engine for the entire European crop protection chemicals industry.

Key Players in the Europe Crop Protection Chemicals Market

The European market is highly competitive and innovation-driven, with strong participation from global and regional leaders. The leading Europe crop protection chemicals companies include:

- BASF SE (Germany)

- Bayer AG (Germany)

- Syngenta (Switzerland)

- FMC Corporation (US)

- Novonesis Group (Denmark)

- Koppert (Netherlands)

- BioFirst Group (Belgium)

- UPL (India)

- Nufarm (Australia)

- Corteva (US)

- American Vanguard Corporation (US)

- Kumiai Chemical Industry Co., Ltd (Japan)

- PI Industries (India)

- Gowan Company (US)

- Albaugh LLC (US)

These companies are actively investing in biologicals, sustainable chemistries, digital farming solutions, precision application systems, and low-residue formulations, reshaping the competitive structure of the European market.

Market Outlook

The Europe crop protection chemicals market is transitioning from volume-driven growth to innovation-led, sustainability-driven expansion. Regulatory alignment, technological advancement, and environmental responsibility are now core growth pillars.

With rising adoption of IPM, biologicals, precision agriculture, and eco-friendly formulations, the market is evolving into a high-value, innovation-centric agricultural ecosystem, supporting long-term food security, productivity, and environmental sustainability across Europe.