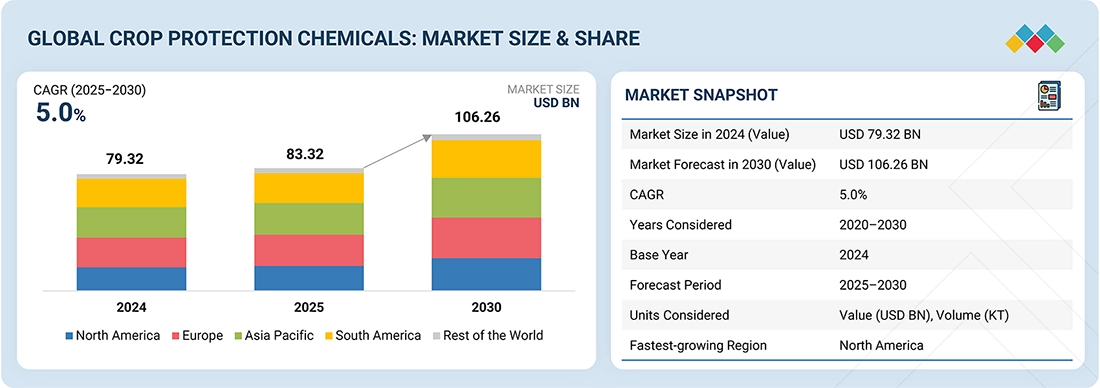

The global crop protection chemical market is witnessing steady expansion, driven by the rising need to safeguard agricultural productivity and meet increasing global food demand. The market is estimated at USD 83.32 billion in 2025 and is projected to reach USD 106.26 billion by 2030, growing at a CAGR of 5.0% during the forecast period (2025–2030).

This growth reflects the growing dependence on advanced agrochemical solutions as farmers face rising challenges from pests, weeds, diseases, labor shortages, and stringent food quality regulations across international markets.

Crop Protection Chemical Market Growth Drivers

Several structural factors are shaping the expansion of the crop protection chemical industry:

- Increasing Global Trade Standards: The expansion of global agricultural trade has significantly raised expectations for quality, appearance, and phytosanitary compliance. Farmers are under pressure to produce export-grade crops with minimal defects and residue compliance, which has accelerated the adoption of crop protection chemicals across farming systems.

- Agricultural Labor Shortages: In many regions, declining availability and rising cost of agricultural labour have pushed farmers toward chemical-based weed and pest management solutions. These inputs offer a more scalable and cost-effective alternative to manual field operations.

- Growth of Organized Agriculture Ecosystems: The rise of contract farming, organised retail, and food processing industries has strengthened demand for uniform, high-quality agricultural produce. This shift is reinforcing the widespread use of crop protection solutions across the value chain.

By Origin: Synthetic Crop Protection Chemicals Dominate the Market

The synthetic crop protection chemicals segment holds the largest share of the market by origin. This dominance is attributed to several key advantages:

- High efficacy and broad-spectrum pest control capabilities

- Reliable and consistent performance across diverse crops and climates

- Rapid action against weeds, insects, and diseases

- Compatibility with large-scale and commercial farming systems

- Cost efficiency per hectare compared to alternative solutions

- Longer shelf life and standardised manufacturing processes

Synthetic herbicides, fungicides, and insecticides remain the preferred choice in commercial agriculture due to their ability to deliver predictable yield protection and operational efficiency.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=380

By Mode of Application: Soil Treatment Holds Strong Demand

The soil treatment segment accounts for a significant share of the market, primarily due to its effectiveness in managing early-stage crop risks. Soil-based application methods help control:

- Soil-borne pathogens

- Nematodes

- Root diseases

Common application practices include soil drenching, seedbed treatment, and root-zone application. These methods improve soil health, enhance nutrient absorption, and promote strong early crop establishment.

Soil treatment approaches are widely adopted in:

- Horticulture crops

- Row crops

- Protected cultivation systems

Their ability to reduce early-stage crop losses makes them an essential component of integrated crop protection strategies.

Regional Analysis: Asia Pacific Leads the Market

The Asia Pacific region holds a dominant share in the global crop protection chemical market, supported by its large agricultural base and intensive farming practices.

Key factors driving regional demand include:

- High dependency on agriculture for rural livelihoods and food security

- Large-scale production of staple crops such as rice, wheat, maize, and pulses

- Year-round cultivation cycles in several countries

- Prevalence of smallholder farming systems requiring frequent crop protection interventions

- Rising population and increasing food consumption

- Government initiatives supporting modern agricultural inputs

Major markets such as China, India, Southeast Asia, and Australia are experiencing strong adoption due to improved access to agrochemicals, expanding distribution networks, and the gradual shift toward modern farming techniques.

Leading Crop Protection Chemicals Companies:

The crop protection chemical market is highly competitive, with key global and regional players focusing on innovation, product expansion, and sustainable agriculture solutions.

Prominent companies operating in the market include:

- BASF SE (Germany)

- Bayer AG (Germany)

- FMC Corporation (US)

- Syngenta Group (Switzerland)

- Corteva (US)

- UPL (India)

- Nufarm (Australia)

- Sumitomo Chemical Co., Ltd. (Japan)

- Albaugh LLC (US)

- Koppert (Netherlands)

- Gowan Company (US)

- American Vanguard Corporation (US)

- Kumiai Chemical Industry Co., Ltd. (Japan)

- PI Industries (India)

- BioFirst Group (Belgium)

These companies are actively investing in R&D, bio-based alternatives, and precision agriculture solutions to strengthen their global market position.