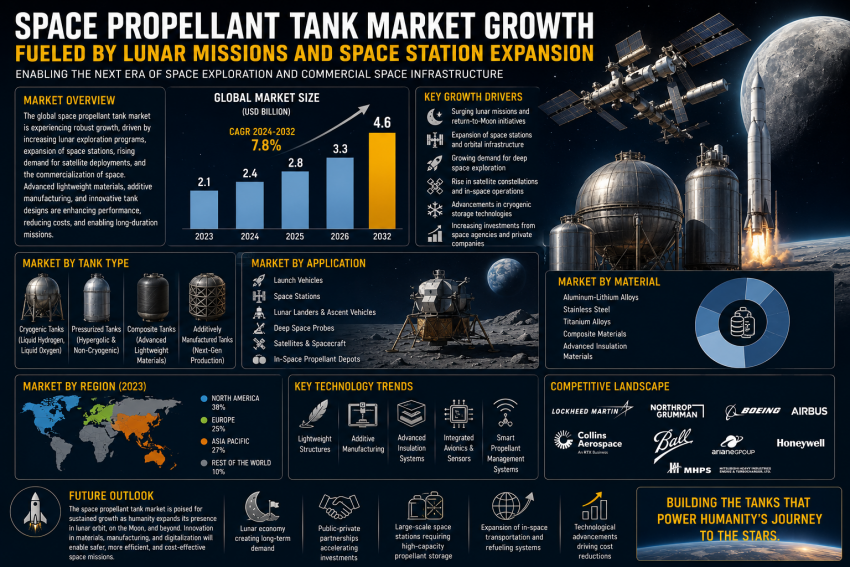

The global space propellant tank market is entering a transformative growth phase as lunar exploration programs, commercial space stations, and reusable launch systems reshape the economics of space operations. Propellant tanks, once viewed as secondary structural components, are now becoming mission-critical technologies that directly influence launch efficiency, spacecraft endurance, refueling capability, and deep-space sustainability. Increasing investments in lunar infrastructure, orbital fuel depots, and long-duration missions are driving unprecedented demand for advanced cryogenic and reusable tank systems across the aerospace ecosystem.

Recent industry projections indicate that the space propellant tank market could exceed USD 4.8 billion by 2030, supported by rising launch cadence, reusable spacecraft architectures, and government-backed lunar exploration initiatives. The market is also benefiting from rapid innovation in lightweight composite materials, methane-fueled propulsion systems, smart fuel-monitoring technologies, and thermal insulation engineering.

One of the most significant catalysts accelerating market growth is the global resurgence of lunar missions. Programs associated with NASA’s Artemis initiative, along with parallel lunar ambitions from China, Europe, India, and private space companies, are creating sustained demand for high-capacity cryogenic propellant storage systems. NASA’s evolving lunar roadmap now emphasizes long-term Moon surface operations and permanent infrastructure, requiring repeated launches, orbital refueling systems, cargo transfer modules, and deep-space landers.

Download PDF Brochure : https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=195002624

The expansion of lunar bases and orbital logistics is dramatically increasing the need for reliable liquid hydrogen, liquid oxygen, and methane storage technologies. These missions require tanks capable of maintaining propellant stability during extended missions under extreme thermal and microgravity conditions. Unlike earlier short-duration missions, modern lunar architectures rely heavily on in-space refueling, reusable landers, and orbital staging systems, all of which depend on advanced propellant containment solutions.

The rise of reusable launch vehicles is another major force reshaping the market. Companies such as SpaceX and Blue Origin are developing next-generation rockets designed for repeated missions with minimal refurbishment. These systems require propellant tanks that can withstand repeated pressure cycles, cryogenic exposure, structural fatigue, and thermal stress. Modern reusable rockets increasingly incorporate composite overwrapped pressure vessels (COPVs), insulated cryogenic tanks, and zero-slosh fuel management systems to improve mission reliability and reduce launch costs.

SpaceX’s latest Starship V3 architecture demonstrates how rapidly tank engineering is evolving. The updated design integrates advanced cryogenic fuel handling, in-orbit fuel transfer capability, and zero-gravity propellant management systems designed specifically for lunar and Mars missions. Such developments are pushing manufacturers to innovate lightweight tank structures with enhanced thermal control and structural durability.

Commercial space station development is also emerging as a powerful market driver. As governments gradually transition from publicly operated orbital stations toward commercial low-Earth-orbit habitats, demand is rising for orbital propulsion modules, fuel storage systems, and station-keeping technologies. Future commercial stations will require periodic refueling and propulsion support, increasing dependence on modular propellant storage systems optimized for long-duration orbital deployment.

Simultaneously, the concept of orbital fuel depots is gaining traction across the industry. Space agencies and private operators increasingly recognize that sustainable lunar and Mars exploration will require large-scale fuel storage and transfer infrastructure in orbit. Online discussions and industry forums have highlighted growing interest in cryogenic fuel depots capable of supporting reusable lunar landers and interplanetary missions. This emerging infrastructure model could create an entirely new segment within the propellant tank market focused on orbital storage, transfer efficiency, and autonomous refueling systems.

Technological advancements are further accelerating adoption. AI-enabled monitoring systems, IoT-connected sensors, and digital twin technologies are improving tank diagnostics, fuel efficiency, and predictive maintenance capabilities. Smart propellant tanks equipped with embedded sensors can continuously monitor temperature, pressure, and structural integrity during missions, reducing operational risk and enhancing mission success rates.

Cryogenic storage technology is becoming especially important as lunar and deep-space missions increasingly rely on liquid hydrogen and methane propulsion systems. Maintaining ultra-low temperatures in space remains one of the most difficult engineering challenges in long-duration missions. As a result, aerospace companies are heavily investing in advanced insulation materials, multilayer thermal protection systems, and active cooling technologies to minimize propellant boil-off and improve fuel retention efficiency.

The growing interest in in-situ resource utilization (ISRU) is also influencing future market opportunities. Researchers and industry experts are actively exploring the possibility of producing oxygen and hydrogen propellants directly from lunar resources. Discussions surrounding lunar water extraction and off-Earth fuel production suggest that future lunar infrastructure could eventually support autonomous propellant manufacturing ecosystems. If commercialized successfully, ISRU could significantly reshape long-term propellant storage requirements and create new demand for lunar-compatible storage and transfer systems.

Defense and national security applications are contributing additional momentum to market expansion. Governments increasingly view space infrastructure as strategically critical, leading to rising investments in military satellites, rapid launch systems, orbital maneuvering platforms, and resilient space logistics. These applications require compact, high-reliability propellant tanks capable of operating under highly demanding mission conditions.

Regionally, North America currently dominates the global space propellant tank market due to strong NASA funding, private-sector launch activity, and defense-related space investments. However, Asia-Pacific is projected to witness the fastest growth during the next decade as China, India, Japan, and South Korea expand lunar programs, launch infrastructure, and commercial satellite deployments.

Competition within the market is intensifying as aerospace manufacturers race to secure positions in the rapidly expanding lunar and commercial space economy. Major players are focusing on lightweight composite tanks, reusable cryogenic systems, additive manufacturing techniques, and autonomous propellant management technologies to gain competitive advantages. Strategic mergers, partnerships, and government contracts are expected to further accelerate innovation and production scale.

Explore In-Depth Industry Analysis: https://www.marketsandmarkets.com/Market-Reports/satellite-propellant-tanks-market-195002624.html

Looking ahead, the future of the space propellant tank market will be closely tied to the success of lunar colonization strategies, reusable launch economics, and orbital infrastructure expansion. As humanity moves toward sustained lunar presence and eventually interplanetary exploration, propellant storage systems will evolve from supportive hardware into foundational infrastructure for the broader space economy.

The convergence of lunar missions, commercial space stations, reusable rockets, and orbital fuel depots is creating a long-term growth environment for the space propellant tank industry. With governments and private companies alike investing aggressively in deep-space logistics and sustainable exploration architectures, advanced propellant tank technologies are poised to become one of the most strategically important segments within the global aerospace and defense market.