The Future of Advanced Counter-Drone Defense in Military and Homeland Security

Summary

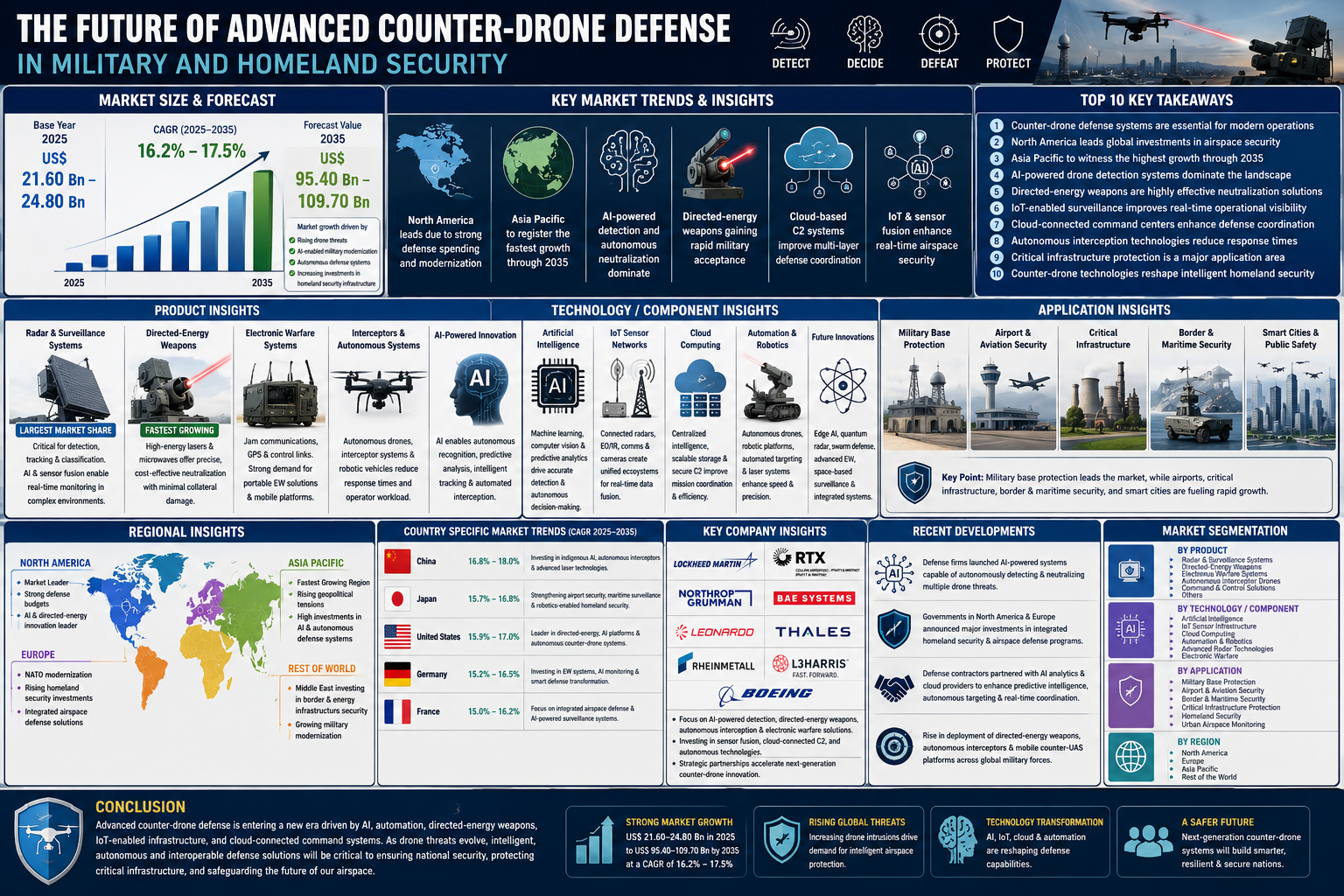

The global Advanced Counter-Drone Defense Market is estimated to grow from US$ 21.60 Billion – US$ 24.80 Billion in 2025 to US$ 95.40 Billion – US$ 109.70 Billion by 2035 at a CAGR of 16.2% – 17.5% from 2025 to 2035. The rapid rise in unauthorized drone activities, evolving asymmetric warfare tactics, and increasing threats to critical infrastructure are accelerating investments in intelligent counter-drone defense systems across military and homeland security sectors. Governments worldwide are prioritizing AI-powered surveillance, autonomous interception systems, directed-energy weapons, advanced radar technologies, and cloud-connected airspace monitoring platforms to strengthen national security preparedness. The market is further supported by the growing integration of artificial intelligence, IoT-enabled sensor networks, automation-driven threat neutralization, and real-time battlefield analytics that enhance situational awareness and operational efficiency. Increasing military modernization programs, border surveillance requirements, airport security concerns, and smart city protection initiatives are expected to drive sustained market expansion through 2035.

Key Market Trends & Insights

North America remains the leading market due to strong defense spending and advanced military modernization initiatives.

Asia Pacific is projected to register the fastest growth driven by rising geopolitical tensions and expanding investments in intelligent defense infrastructure.

AI-powered drone detection and autonomous threat neutralization systems dominate current technology adoption trends.

Directed-energy weapons such as high-energy lasers and microwave systems are gaining rapid military acceptance.

Cloud-based command-and-control systems are improving operational coordination across multi-layer defense networks.

Automation and IoT-enabled sensor fusion technologies are enhancing real-time airspace security and threat intelligence.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=4197284

Market Size & Forecast

- Base year market size (2025): US$ 21.60 Billion – US$ 24.80 Billion

- Forecast value by 2035: US$ 95.40 Billion – US$ 109.70 Billion

- CAGR (2025–2035): 16.2% – 17.5%

- Market growth is fueled by rising drone threats, AI-enabled military modernization, autonomous defense systems, and increasing investments in homeland security infrastructure

The Future of Advanced Counter-Drone Defense in Military and Homeland Security Top 10 key takeaway

- Counter-drone defense systems are becoming essential for modern military and homeland security operations

- North America leads global investments in advanced airspace security technologies

- Asia Pacific is expected to witness the highest growth through 2035

- AI-powered drone detection systems dominate the defense modernization landscape

- Directed-energy weapons are emerging as highly effective drone neutralization solutions

- IoT-enabled surveillance systems are improving real-time operational visibility

- Cloud-connected command centers are enhancing defense coordination capabilities

- Autonomous interception technologies are reducing response times significantly

- Critical infrastructure protection is becoming a major application area

- Counter-drone technologies are reshaping the future of intelligent homeland security systems

Product Insights

Radar and surveillance systems currently account for the largest share of the advanced counter-drone defense market due to their critical role in drone detection, tracking, and classification. Modern radar systems equipped with AI-based analytics and sensor fusion capabilities can identify low-signature drones operating in complex urban and battlefield environments. Their ability to provide continuous real-time monitoring across large operational zones makes them indispensable for military installations, airports, and critical infrastructure facilities.

Directed-energy weapon systems are rapidly emerging as one of the fastest-growing product categories within the market. High-energy laser systems and microwave-based platforms offer cost-effective drone neutralization with precision targeting capabilities and minimal collateral damage. Defense organizations increasingly prefer directed-energy solutions because they provide scalable, repeatable, and low-cost engagement capabilities against drone swarms and fast-moving aerial threats.

Electronic warfare systems are also gaining strong momentum as they enable military operators to jam drone communication frequencies, GPS signals, and onboard control systems. Portable anti-drone rifles, mobile interceptor platforms, and autonomous defense vehicles are witnessing rising deployment across border surveillance and homeland security applications.

AI integration continues to transform product innovation by enabling autonomous target recognition, predictive threat analysis, intelligent tracking, and automated interception capabilities. Manufacturers are increasingly focusing on lightweight, mobile, and interoperable counter-drone systems capable of operating across diverse mission environments.

Technology / Component Insights

Artificial intelligence remains the foundational technology driving innovation across advanced counter-drone defense systems. Machine learning algorithms, computer vision platforms, neural networks, and predictive analytics tools are enabling highly accurate drone detection and autonomous decision-making in real-time operational environments.

IoT-enabled sensor networks are significantly improving airspace monitoring capabilities by connecting radars, electro-optical systems, communication platforms, surveillance cameras, and command centers into unified operational ecosystems. Connected defense infrastructure enhances situational awareness while enabling rapid data exchange across multiple defense layers.

Cloud computing technologies are increasingly supporting modern homeland security and military operations by enabling centralized intelligence management, scalable data storage, AI-driven analytics, and secure communication networks. Cloud-based command systems improve mission coordination and operational efficiency during complex counter-drone engagements.

Automation technologies are transforming the market through autonomous surveillance drones, robotic interception platforms, automated laser targeting systems, and intelligent electronic warfare solutions. These technologies reduce operator workload while improving engagement speed and operational precision.

Future innovations are expected to include edge AI processing, quantum-enhanced radar systems, autonomous swarm defense networks, advanced electronic warfare algorithms, and integrated space-based surveillance infrastructure. These advancements will redefine intelligent airspace security and autonomous defense operations during the next decade.

Application Insights

Military base protection remains the leading application segment within the advanced counter-drone defense market. Rising concerns over drone-enabled reconnaissance missions, aerial attacks, and electronic warfare threats are compelling governments to strengthen perimeter security using AI-powered detection and autonomous interception systems.

Airport and aviation security applications are witnessing rapid growth as drone-related disruptions near commercial airports continue to increase globally. Airports are deploying advanced radar systems, AI-enabled airspace monitoring platforms, and automated drone neutralization technologies to ensure safe flight operations and regulatory compliance.

Critical infrastructure protection is becoming a major growth area for counter-drone technologies. Energy facilities, government buildings, communication networks, transportation hubs, and industrial sites are increasingly adopting intelligent airspace protection systems to defend against unauthorized aerial intrusions and cyber-enabled drone threats.

Border surveillance and maritime security applications are also expanding rapidly. Governments are investing in mobile anti-drone systems, autonomous surveillance towers, and integrated sensor networks to improve territorial monitoring and maritime defense capabilities.

Future opportunities are expected to emerge from smart city security initiatives, urban air mobility infrastructure, public event protection, and integrated civil-military airspace management systems.

Regional Insights

North America dominates the advanced counter-drone defense market due to strong defense budgets, early adoption of AI-powered defense systems, and large-scale investments in autonomous military technologies. The United States continues to lead global innovation through the deployment of directed-energy weapons, cloud-connected command platforms, and AI-driven battlefield analytics systems.

Europe is witnessing substantial market growth driven by NATO modernization programs, rising investments in homeland security, and increasing demand for integrated airspace defense solutions. Countries such as Germany, France, and the United Kingdom are strengthening intelligent defense infrastructure to improve national security preparedness.

Asia Pacific is expected to witness the fastest growth through 2035 due to rising geopolitical tensions, military modernization initiatives, and growing investments in AI-enabled defense technologies. China, Japan, India, and South Korea are heavily investing in autonomous surveillance infrastructure, advanced radar systems, and intelligent counter-UAS platforms.

The Middle East is also emerging as a strategically important market because of increasing investments in border security, energy infrastructure protection, and military modernization initiatives.

- North America leads global innovation in intelligent counter-drone systems

- Asia Pacific is projected to register the fastest market growth through 2035

- Europe is strengthening integrated homeland security infrastructure

- AI-powered surveillance technologies are driving regional defense modernization

- Autonomous airspace protection systems are becoming critical for national security strategies

Country Specific Market Trends

China is expected to witness a CAGR of 16.8% – 18.0% from 2025 to 2035 due to expanding investments in indigenous AI-powered defense systems, autonomous drone interception platforms, and advanced laser technologies. The country continues to prioritize military digitalization and intelligent battlefield modernization.

Japan is strengthening airport security systems, maritime surveillance infrastructure, and robotics-enabled homeland security capabilities. AI and automation technologies remain central to national defense modernization strategies.

The United States remains the largest market globally with a CAGR of 15.9% – 17.0% due to continued Pentagon investments in directed-energy systems, AI-enabled surveillance platforms, and autonomous counter-drone technologies. Canada is expanding critical infrastructure protection programs, while Mexico is increasing investments in border security modernization.

Germany and France are investing heavily in integrated electronic warfare systems, AI-powered airspace monitoring, and smart military surveillance technologies to strengthen European defense readiness.

- China is rapidly expanding AI-enabled counter-drone defense infrastructure

- Japan is prioritizing autonomous homeland security modernization programs

- The United States remains the global leader in intelligent airspace defense

- Germany and France are accelerating smart defense transformation initiatives

- Counter-drone technologies are becoming strategic priorities across global security sectors

Key Company Insights

Major companies operating in the advanced counter-drone defense market include Lockheed Martin, RTX Corporation, Northrop Grumman, BAE Systems, Leonardo, Thales Group, Rheinmetall, L3Harris Technologies, and Boeing.

These companies are focusing on AI-powered detection systems, autonomous threat neutralization platforms, directed-energy weapons, and integrated electronic warfare technologies to strengthen competitive positioning. Strategic investments in sensor fusion, predictive analytics, cloud-connected command infrastructure, and autonomous interception capabilities are accelerating product innovation across the industry.

Defense manufacturers are also prioritizing compact, scalable, and mobile counter-drone systems suitable for military operations, homeland security applications, airport defense, and critical infrastructure protection.

- AI-powered surveillance and targeting remain major innovation priorities

- Directed-energy weapons are gaining significant defense industry attention

- Cloud-connected battlefield management systems are improving operational coordination

- Companies are investing heavily in autonomous interception technologies

- Strategic partnerships are accelerating next-generation defense innovation

Recent Developments

Several defense companies recently introduced AI-powered counter-drone systems capable of autonomously identifying and neutralizing multiple aerial threats simultaneously.

Governments across North America and Europe announced increased investments in integrated homeland security infrastructure and advanced airspace defense modernization programs.

Major defense contractors entered strategic partnerships with AI analytics providers and cloud computing companies to improve autonomous targeting, predictive threat intelligence, and real-time operational coordination capabilities.

Market Segmentation

The advanced counter-drone defense market is segmented by product, technology/component, application, and region. By product, the market includes radar systems, directed-energy weapons, electronic warfare platforms, autonomous interceptor drones, surveillance systems, and command-and-control solutions. Radar and surveillance systems currently dominate due to their essential role in real-time threat detection and airspace monitoring.

By technology/component, the market includes artificial intelligence, IoT-enabled sensor infrastructure, cloud computing platforms, robotics, automation systems, advanced radar technologies, and electronic warfare capabilities. AI-enabled analytics and autonomous targeting technologies are projected to witness the highest growth during the forecast period.

Applications include military base protection, airport security, border surveillance, maritime security, homeland security, critical infrastructure protection, and urban airspace monitoring. Military and homeland security applications remain dominant due to rising drone-related threats worldwide.

Regionally, the market is segmented into North America, Europe, Asia Pacific, and the rest of the world. North America currently leads the market, while Asia Pacific is expected to emerge as the fastest-growing region through 2035.

- Radar systems remain critical for advanced drone detection operations

- AI-enabled autonomous targeting technologies are accelerating market growth

- Homeland security applications are witnessing strong demand globally

- Cloud-based command infrastructure is improving defense coordination

- Asia Pacific is becoming a major hub for intelligent airspace defense investments

Conclusion

The future of advanced counter-drone defense in military and homeland security will be defined by intelligent automation, AI-powered surveillance, autonomous interception technologies, and integrated battlefield coordination capabilities. As drone warfare, aerial espionage, and unauthorized airspace intrusions continue to evolve, governments and defense organizations are rapidly investing in next-generation counter-UAS systems to strengthen national security preparedness.

Artificial intelligence, IoT-enabled defense infrastructure, cloud-connected command systems, and autonomous targeting technologies are transforming modern airspace security by enabling faster operational response, predictive threat analysis, and scalable defense capabilities. The growing importance of cost-effective, automated, and cyber-resilient defense systems is expected to support strong market expansion through 2035.

Companies capable of delivering interoperable, AI-driven, and highly autonomous counter-drone solutions will remain strategically positioned to capitalize on rising global demand for intelligent homeland security and military defense technologies.