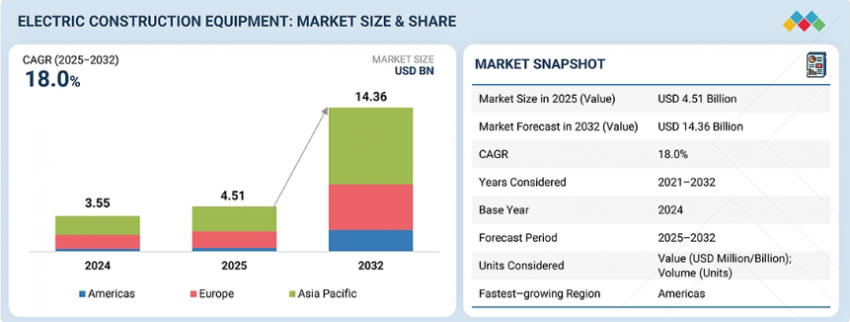

The Electric Construction Equipment Industry is witnessing rapid transformation, with the market projected to grow from USD 4.51 billion in 2025 to USD 14.36 billion by 2032, registering a CAGR of 18.0%. This strong growth trajectory reflects increasing global efforts toward sustainability, electrification, and reduced carbon emissions across construction and mining activities. The rising Electric Construction Equipment Market Share of electric excavators, loaders, and dump trucks highlights a clear shift away from traditional diesel-powered machinery.

Despite strong growth potential, the Electric Construction Equipment Industry faces several challenges that could restrain adoption. One of the primary barriers is the higher upfront cost of electric equipment, which is approximately 1.75 times more expensive than conventional diesel-powered machinery. This cost sensitivity is particularly evident in emerging markets such as India and Indonesia. Additionally, the lack of adequate charging infrastructure—especially in remote or rural construction sites—continues to limit market penetration in the Asia Pacific region.

Battery technology also presents certain limitations. Current systems often restrict operating range and battery life, particularly for heavy-duty applications. Early electric excavators and loaders introduced by Komatsu and Volvo required frequent recharging, impacting productivity. However, ongoing advancements in battery efficiency, combined with expanding charging infrastructure and supportive government policies, are expected to significantly boost the Electric Construction Equipment Market Share in the coming years.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=129288251

Electric Excavators Leading the Market

Electric excavators are expected to dominate the market by type, contributing significantly to the overall Electric Construction Equipment Market Share. These machines are gaining traction due to their economic and environmental advantages. Excavators alone account for over 50% of greenhouse gas emissions on construction sites, making them a key target for electrification.

Stringent emission regulations such as EU Stage V standards are pushing contractors to adopt cleaner alternatives. Electric excavators offer up to 50% savings in fuel and maintenance costs compared to diesel-powered equipment. Furthermore, urban construction projects increasingly demand low-noise solutions. Electric mini excavators operate significantly quieter—often at least 10 dB lower than diesel variants—making them ideal for city environments with strict noise regulations.

Their compact size and suitability for repetitive, short-duration tasks further enhance their adoption, reinforcing their leading position within the Electric Construction Equipment Industry.

Li-NMC Batteries Driving Growth in Asia Pacific

The lithium nickel manganese cobalt oxide (Li-NMC) segment is expected to witness the fastest growth in Asia Pacific, contributing to an expanding Electric Construction Equipment Market Share. This growth is fueled by rising demand for high-performance batteries in construction, mining, and electric mobility applications.

Countries such as China, South Korea, and Japan are heavily investing in battery manufacturing and R&D. Li-NMC batteries offer higher energy density, improved thermal stability, and longer lifecycle compared to conventional lithium-ion batteries. These advantages translate into longer operating hours, reduced downtime, and lower total cost of ownership.

Although Li-NMC batteries are typically 10–20% more expensive due to raw material costs like cobalt and nickel, their superior performance makes them the preferred choice for heavy-duty applications. Leading OEMs such as Komatsu, Hitachi, SANY, and Volvo are increasingly integrating Li-NMC batteries into their latest electric equipment models, accelerating innovation within the Electric Construction Equipment Industry.

Europe Leading the Global Market

Europe is expected to hold the largest Electric Construction Equipment Market Share in 2025, driven by strong regulatory frameworks and ambitious climate goals. Electric excavators and wheel loaders alone are projected to account for over 80% of the regional market.

Cities such as Oslo, Copenhagen, Helsinki, and Stockholm are leading the transition toward zero-emission construction. For instance, Oslo mandates zero-emission public construction sites by 2025, while Copenhagen aims for carbon-neutral construction by 2030. These initiatives are significantly boosting demand within the Electric Construction Equipment Industry.

Additionally, regulations such as Germany’s Stage V emission standards and France’s Climate and Resilience Law are accelerating adoption. OEMs including Caterpillar, Volvo, JCB, Liebherr, Komatsu, and Hitachi are expanding their electric product portfolios and showcasing innovations at major industry events like Bauma and Intermat.

Competitive Landscape

Key players shaping the Electric Construction Equipment Industry include Caterpillar Inc., Komatsu Ltd., Volvo Construction Equipment, Hitachi Construction Machinery Co., Ltd., JCB, Epiroc AB, Sandvik AB, Liebherr, Doosan Group, Soletrac Inc., and Dana Limited. These companies are actively investing in electrification technologies, battery advancements, and strategic partnerships to strengthen their global Electric Construction Equipment Market Share.

Request Sample Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=129288251