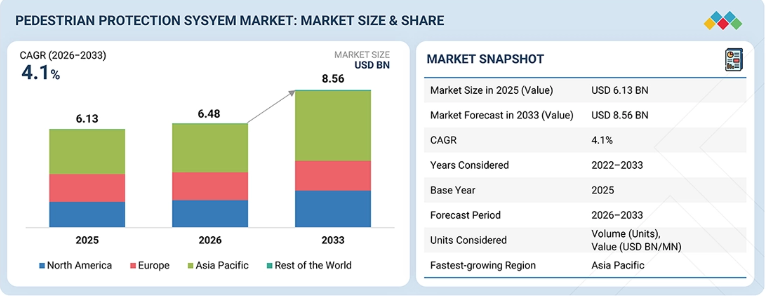

The Pedestrian Protection System Market is projected to reach USD 8.56 billion by 2033 from USD 6.48 billion in 2026, at a CAGR of 4.1% during the forecast period.

Growing regulatory analysis and OEM safety mandates are prompting automakers to invest in advanced pedestrian protection systems. Radar and camera-based solutions allow real-time detection and system validation while supporting data-driven safety performance monitoring, thereby reducing liability risks. As regulatory pressure rises and pedestrian safety becomes a key differentiator, the adoption of automated safety systems such as pedestrian automatic emergency braking and active hood lift is increasing across both developed and emerging markets.

By EV type, BEVs secure the leading position during the forecast period.

BEVs are expected to hold the largest share in the pedestrian protection system market due to the global trend of electrification and the rapid adoption of electric vehicles with advanced safety technologies. These vehicles are built on a separate architecture that allows more flexibility in designing the front-end structure to optimize sensor and actuator placement. Vehicles like Tesla Model 3 and Model Y, BYD Atto 3, and Hyundai IONIQ 5 are increasingly integrating advanced pedestrian protection and AEB systems. Suppliers such as Bosch, Denso, Valeo, and Aumovio are also developing compact, energy-efficient pedestrian protection systems for electric vehicles.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=253754061

In the component segment, cameras rank second during the forecast period.

In the pedestrian protection system market, cameras are becoming essential because of their ability to provide accurate pedestrian detection and classification in real time. Their growth is driven by the rapid adoption of ADAS, where cameras are the main sensing layer for perception. Cameras allow precise identification of vulnerable road users through AI-based object recognition, lane context understanding, and trajectory prediction in busy urban areas. OEMs are focusing on cameras for better decision accuracy and fewer false positives when combined with braking systems. For instance, Bosch is upgrading its MPC camera platforms with AI-driven perception. Similarly, Valeo is working on high-resolution front cameras with a wider field of view. Denso is also enhancing vision sensors for better low-light performance. These innovations are strengthening detection reliability and response performance across vehicle platforms.

Regulatory mandates and safety rating programs accelerate pedestrian protection adoption in North America.

The pedestrian protection systems market in North America is expanding, influenced by regulations and rating systems that impact system design, validation, and feature deployment. IIHS has improved its testing criteria by adding assessments of the vehicle’s AEB capabilities, including detection and braking during daytime and nighttime conditions. This includes crossing and parallel pedestrian motion, with higher ratings awarded for better low-light detection and braking. NHTSA is also moving toward formalizing the inclusion of pedestrian AEB systems in the New Car Assessment Program, focusing on forward collision avoidance features. This shift impacts OEMs, who now must enhance sensor fusion accuracy, detection ranges over 40 m, and critical response times for AEB systems, which are being integrated into vehicles like the Ford F-150, Toyota Highlander, and Honda CR-V.

Key Players

Major players in the pedestrian protection system market include Robert Bosch GmbH (Germany), Aumovio (Germany), Denso Corporation (Japan), ZF Group (Germany), and Aptiv (Ireland). These companies have been adopting various strategies to maintain their market positions. The main strategies used are product launches, deals, and expansions. These strategies have been analyzed to understand each company’s standing in the market.

Request Free Sample Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=253754061