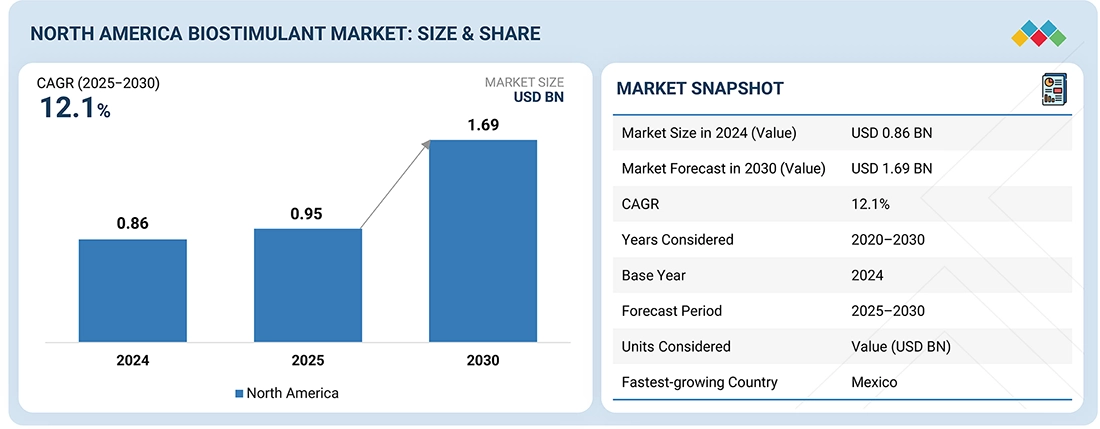

The North America biostimulant market is positioned for strong and sustained expansion, driven by the rapid evolution of sustainable agriculture and biological crop enhancement technologies. The market is projected to grow from USD 0.95 billion in 2025 to USD 1.69 billion by 2030, registering a robust CAGR of 12.1% during the forecast period. This growth trajectory reflects the increasing commercial value and strategic importance of the North America biostimulants market as biological inputs become central to modern crop productivity systems.

This expansion also highlights the structural transformation of the North America biostimulants industry, as farmers and agribusinesses shift away from conventional chemical dependency toward eco-efficient, performance-driven biological solutions that support soil regeneration, climate resilience, and yield optimization.

Market Growth Drivers: Sustainability, Soil Health & Climate Resilience

The growth of the biostimulants market across North America is driven by multiple long-term structural and agronomic forces:

- Rising focus on soil health management

- Increasing climate variability and abiotic stress conditions

- Demand for nutrient-use efficiency and yield stability

- Shift toward sustainable and low-impact agricultural inputs

- Expansion of regenerative and precision farming systems

Biostimulants contribute directly to improved agricultural performance by enhancing:

- Root system development

- Plant stress tolerance (drought, salinity, temperature fluctuations)

- Nutrient absorption efficiency

- Yield consistency and crop quality

The expanding adoption of microbial-based, seaweed-derived, and amino acid-based formulations is accelerating application scalability across diverse crop systems. At the same time, integration with precision agriculture platforms, agritech tools, and digital farm management systems is enabling targeted, data-driven deployment across both smallholder and commercial farming operations.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=14377455

Liquid Biostimulants Segment: Market Leadership by Form

The liquid biostimulants segment dominates the North America biostimulant market by form due to its operational efficiency and agronomic performance advantages:

- Ease of handling and storage

- Rapid plant absorption

- Compatibility with existing crop management infrastructure

- Precision dosing and uniform distribution

Liquid biostimulants enable application through:

- Foliar spraying systems

- Fertigation infrastructure

- Seed treatment technologies

Their versatility across crop types, combined with advancements in formulation stability, bioactive compound delivery systems, and biological efficacy, positions liquid formulations as the preferred commercial format among farmers and agribusiness operators.

Cereals & Grains Segment: High-Volume Growth Engine

The cereals and grains segment represents one of the largest revenue-generating crop categories in the North America biostimulant market. Extensive cultivation of corn, wheat, and barley across the region creates sustained demand for biological crop enhancement solutions.

Biostimulants improve cereal productivity by:

- Enhancing nutrient uptake efficiency

- Improving root architecture and soil interaction

- Increasing resistance to environmental stress

- Improving yield stability under intensive farming systems

As climate pressure and soil degradation intensify, biostimulants are becoming structurally embedded within large-scale cereal production strategies, supported by targeted formulations and validated agronomic performance.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=14377455

Canada’s Role in Regional Market Expansion

Canada plays a strategic role in regional market growth, supported by:

- A technologically advanced agricultural sector

- Strong policy emphasis on sustainable farming practices

- Rising adoption of eco-friendly crop inputs

- Expansion of regenerative agriculture models

Canadian farmers are increasingly using biostimulants to:

- Improve soil biological activity

- Enhance nutrient-use efficiency

- Increase crop resilience to drought, cold stress, and salinity

Key crops, including cereals, oilseeds, and horticultural products, benefit from microbial, seaweed-based, and amino acid-derived formulations. Supportive government programs, expanding distribution networks, and agronomic education initiatives strengthen Canada’s leadership position in the regional market ecosystem.

Competitive Landscape: North America Biostimulants Companies

The North America biostimulants market features a highly competitive ecosystem of global and regional agriscience leaders, shaping innovation, commercialization, and market consolidation. Major North American biostimulants companies include:

- Nutrien Ltd (Canada)

- Syngenta AG (Switzerland)

- BASF SE (Germany)

- Bayer AG (Germany)

- Corteva Agriscience (US)

- Lallemand Plant Care (Canada)

- Acadian Seaplants Limited (Canada)

- Koppert Biological Systems B.V. (Netherlands)

- Seipasa S.A. (Spain)

- Tradecorp International S.A. (Spain)

- Novonesis A/S (Denmark)

- Koppert Biological Systems B.V. (Netherlands)

- Brandt Consolidated, Inc. (US)

- Valagro S.p.A. (Italy)

- FMC Corporation (US)

These players are investing heavily in biological R&D, sustainable formulation development, precision-agriculture integration, and strategic distribution partnerships, intensifying competition and accelerating the maturity of the market.

Market Outlook

With rising sustainability regulations, climate volatility, and demand for productivity-linked biological inputs, the North America biostimulants market is transitioning from an emerging segment to a core pillar of modern agricultural systems. Long-term growth will be driven by:

- Regulatory support for biological inputs

- Expansion of regenerative agriculture

- Integration with digital farming ecosystems

- Commercial adoption by large-scale agribusiness operations

- Strong institutional and private-sector investment

This positions biostimulants as a foundational component of the future North American agricultural value chain.