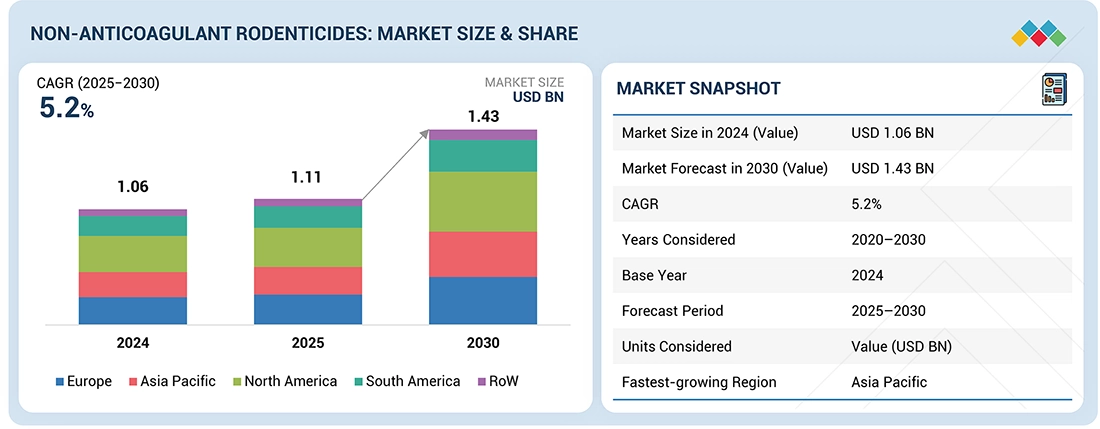

The global non-anticoagulant rodenticides market is expected to grow from USD 1.11 billion in 2025 to USD 1.43 billion by 2030, registering a CAGR of 5.2% during the forecast period.

Market growth is being driven primarily by the increasing resistance of rodents to anticoagulant rodenticides and the tightening of regulations governing conventional rodent control products. Rapid urbanization, expansion of food-processing industries, and intensified agricultural activity are further fueling demand for fast-acting and highly effective rodent control solutions. Non-anticoagulant products such as zinc phosphide, bromethalin, and cholecalciferol are increasingly favored due to their rapid mode of action and comparatively lower risk of secondary poisoning. Additionally, stringent food safety and environmental standards are accelerating the shift toward low-residue and environmentally responsible formulations. Ongoing technological advancements—including microencapsulation, enhanced bait palatability, and sensor-enabled smart baiting systems—are improving efficacy while reducing non-target exposure, supporting adoption across urban, industrial, and agricultural applications worldwide.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=13299457

Zinc Phosphide Dominates the Type Segment

Zinc phosphide accounts for a significant share of the non-anticoagulant rodenticides market by type, supported by its proven effectiveness, rapid action, and cost efficiency. It is widely used across agriculture, food storage facilities, and urban pest management due to its ability to deliver quick mortality while minimizing bait shyness and reducing crop or inventory losses. Its adaptability across various bait formulations and broad availability further strengthen its market position. Rising rodent resistance to anticoagulants and stricter regulatory controls on traditional rodenticides continue to drive increased adoption of zinc phosphide–based products, reinforcing its leadership in this segment. Key market participants operating in this space include BASF (Germany), Sumitomo Chemical (Japan), UPL Ltd./Arysta LifeScience (India), Bell Laboratories, Inc. (US), and PCT Rural (Australia).

Pellets Lead the Mode of Application Segment

The pellets segment holds a substantial share of the market owing to its operational efficiency, ease of application, and high effectiveness. Pellet formulations enable precise dosing, are easy to handle, and offer high palatability, ensuring reliable rodent control in both agricultural and urban environments. Commonly used with zinc phosphide, bromethalin, and cholecalciferol, pellets provide targeted and rapid action. Their superior stability and longer shelf life compared to powders or liquid formulations enhance usability for pest control professionals. Furthermore, their compatibility with automated baiting systems and integrated pest management (IPM) programs continues to reinforce pellets as the dominant application mode in the non-anticoagulant rodenticides market.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=13299457

North America Holds a Significant Regional Share

North America represents a significant share of the global non-anticoagulant rodenticides market, driven by increasing rodent resistance to anticoagulants, stringent food safety and environmental regulations, and widespread adoption of acute toxicants such as zinc phosphide, bromethalin, and cholecalciferol. The region’s extensive urban infrastructure, large-scale food-processing operations, and well-developed agricultural sector generate sustained demand for fast and reliable rodent control solutions. Additionally, the presence of leading market players and the early adoption of advanced pest management technologies—including pellet-based formulations and smart baiting systems—further support North America’s strong market position.

Competitive Landscape

The market features a diverse mix of global and regional players actively engaged in the development, manufacturing, and distribution of non-anticoagulant rodenticides. Key companies profiled in the report include BASF (Germany), Sumitomo Chemical (Japan), UPL Ltd (India), Bell Laboratories, Inc. (US), PCT Rural (Australia), Animal Control Technologies (Australia), Imtrade CropScience (Australia), Rentokil Initial plc (UK), AG Schilling & Co (Germany), 4Farmers Australia (Australia), Farmalynx Pty Ltd (Australia), Zagro (Malaysia), JT Eaton & Co., Inc. (USA), Neogen Technologies (USA), and Liphatech, Inc. (US). These companies play a critical role in supplying zinc phosphide, bromethalin, cholecalciferol, and other non-anticoagulant solutions across agricultural, urban, and industrial markets worldwide.