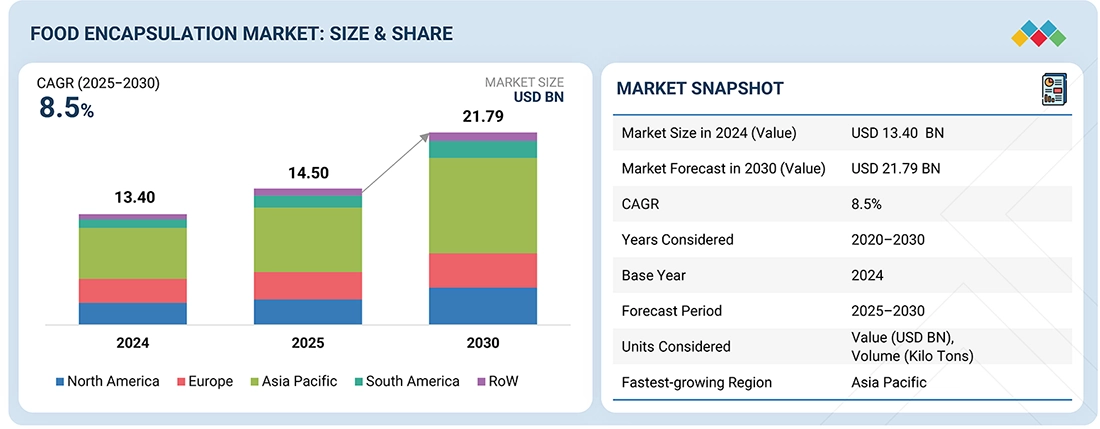

The global food encapsulation market is witnessing strong growth, reflecting the increasing demand for functional, stable, and high-performance food ingredients. Valued at USD 14.50 billion in 2025, the market is projected to reach USD 21.79 billion by 2030, expanding at a CAGR of 8.5%. This growth trajectory highlights the critical role encapsulation technologies play in modern food processing and nutrition delivery systems.

What is Food Encapsulation and Why It Matters

Food encapsulation refers to the technique of enclosing active ingredients—such as vitamins, minerals, flavors, probiotics, and bioactives—within a protective coating or shell. This process safeguards sensitive components from environmental stressors like heat, moisture, oxygen, and processing conditions.

As a result, encapsulation ensures:

- Improved ingredient stability

- Enhanced shelf life

- Controlled release of nutrients

- Consistent product performance

These advantages make encapsulation indispensable across applications such as functional foods, dietary supplements, infant nutrition, and pet food.

Food Encapsulation Market Growth Drivers

- Rising Demand for Functional and Preventive Nutrition: Consumers are increasingly shifting toward health-focused, clean-label, and preventive food products. Encapsulation enables manufacturers to deliver bioactive ingredients effectively while maintaining taste, texture, and nutritional value.

- Technological Advancements: Innovations in encapsulation technologies—such as spray drying, fluid-bed coating, coacervation, and lipid-based systems—are improving scalability, efficiency, and cost-effectiveness. These advancements are making encapsulation more accessible for large-scale food production.

- Growth in Fortified Foods and Supplements: Encapsulation plays a pivotal role in micronutrition by enhancing the delivery and bioavailability of essential nutrients like omega-3 fatty acids, vitamins, and minerals.

Competitive Landscape and Key Players

Leading global companies are actively investing in R&D, formulation stability, and capacity expansion to strengthen their market position. Major players include:

- Nestlé

- Danone

- Kerry Group

- DSM-Firmenich

- Ingredion

- BASF

- Cargill

Additional key contributors include:

- Givaudan

- International Flavors & Fragrances

- Archer Daniels Midland

- Tate & Lyle

- Sensient Technologies

These companies are focusing on application-specific encapsulated solutions and process optimization to meet evolving industry demands.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=68

Segment Insights

By Shell Material: Polysaccharides Lead the Market

Polysaccharides dominate the food encapsulation market due to their:

- Broad regulatory acceptance

- Functional versatility

- Compatibility with various food systems

Common materials include maltodextrin, modified starch, gum arabic, alginate, pectin, and cellulose derivatives. Their ability to form protective films and stabilize sensitive ingredients makes them ideal for large-scale applications.

Additionally, polysaccharides support:

- Clean-label formulations

- Plant-based positioning

- Controlled release mechanisms

- Sensory neutrality in food products

By Technology: Microencapsulation Takes the Lead

Microencapsulation holds the largest market share owing to its:

- Proven reliability

- Cost-effectiveness

- Ease of integration into existing food processing systems

Widely used techniques include spray drying, fluidized bed coating, coacervation, and extrusion.

Key benefits:

- Protection of sensitive ingredients

- Controlled release functionality

- Taste masking and odor control

- Improved shelf life and handling

Compared to nanoencapsulation, microencapsulation offers a clearer regulatory pathway and is more suitable for food-grade applications.

Regional Analysis: North America Dominates

North America accounts for the largest share of the global food encapsulation market, driven by:

- A mature functional food ecosystem

- High consumer awareness of nutraceuticals

- Strong presence of leading food and ingredient companies

The United States plays a central role, with widespread use of encapsulated ingredients across dietary supplements, fortified foods, and clinical nutrition.

Additional factors supporting regional dominance include:

- Advanced food processing infrastructure

- Early adoption of encapsulation technologies

- Well-established regulatory frameworks

Major companies such as Archer Daniels Midland, Cargill, and Ingredion maintain strong R&D and manufacturing capabilities in the region.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=68

Emerging Opportunities in the Asia Pacific

While North America and Europe remain established markets, the Asia Pacific is emerging as a high-growth region. Key growth drivers include:

- Rapid urbanization

- Increasing health awareness

- Rising demand for fortified and functional foods

This region is expected to witness significant investments and expansion activities from global players.

Future Outlook

Food encapsulation is set to remain a cornerstone technology in the evolution of the food and nutrition industry. As demand for personalized nutrition, clean-label products, and sustainable food systems continues to rise, encapsulation will play a critical role in:

- Enhancing nutrient delivery and bioavailability

- Enabling product innovation and differentiation

- Supporting regulatory compliance and quality standards

With continuous advancements in encapsulation techniques and increasing industry adoption, the market is poised for sustained growth in the coming years.