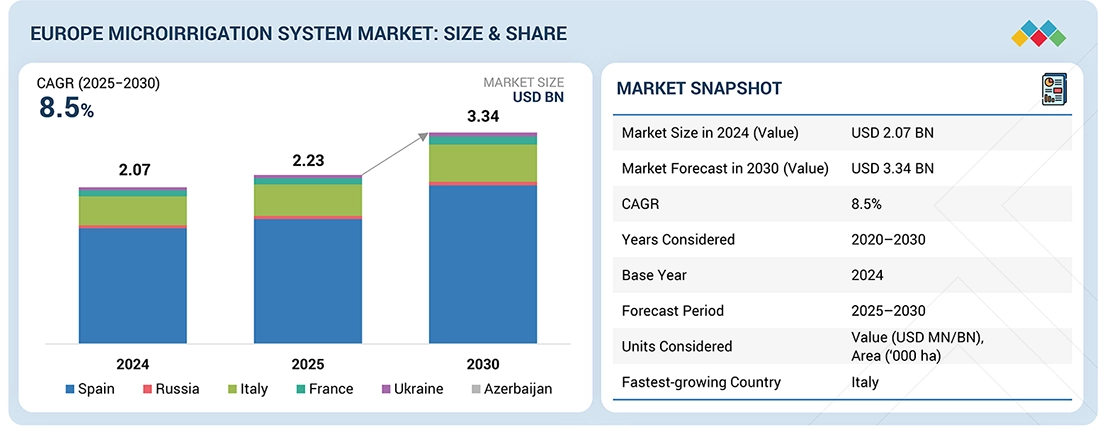

The Europe microirrigation system market is poised for sustained expansion, projected to grow from USD 2.23 billion in 2025 to USD 3.34 billion by 2030, registering a CAGR of 8.5% during the forecast period. The Europe Microirrigation System Industry is increasingly recognizing microirrigation as a core component of modern agricultural infrastructure, driven by intensifying water scarcity, stricter regulatory frameworks on water usage, and the need for long-term farm productivity and profitability. These structural shifts clearly define the Europe Microirrigation System Market Drives, where regulatory compliance, climate resilience, and precision water management are becoming strategic imperatives for European agriculture.

Market Drivers: Regulation, Water Efficiency, and Climate Variability

European agriculture is undergoing a structural transition from traditional irrigation models toward precision-driven water management systems. Governments across the region are enforcing tighter water-use regulations, compelling farmers to upgrade legacy flood and sprinkler systems in favor of more accurate, efficient, and sustainable microirrigation technologies.

This transition is not just about reducing water consumption—it is about maximizing yields, minimizing variable input costs, and stabilizing production under climate uncertainty. Increasing weather volatility is forcing growers to synchronize irrigation and nutrient delivery with crop growth stages and soil conditions at a highly localized level. As a result, microirrigation is evolving from a cost-saving tool into a strategic productivity and risk-management asset.

Regulatory pressure, water pricing mechanisms, and resource scarcity are accelerating the phase-out of conventional irrigation methods. Farms that fail to modernize risk losing access to water resources, public support programs, and competitive market positioning—making microirrigation adoption not optional, but essential for long-term sustainability.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=222332152

Supplier Transformation: From Equipment Vendors to Solution Providers

European microirrigation suppliers are repositioning themselves as integrated solution providers rather than standalone equipment sellers. By offering bundled services such as automation, digital monitoring, agronomic advisory services, preventive maintenance, service contracts, flexible system design, phased installations, and financing models, they are building long-term customer relationships and recurring revenue streams.

This ecosystem approach is lowering adoption barriers for mid-sized farms, enabling access to advanced irrigation technologies that were previously limited to large commercial operations. The result is a positive feedback loop supporting stable, long-term market growth.

Microsprinkler Systems: Fastest-Growing Segment (2025–2030)

By type, the microsprinkler segment is projected to be the fastest-growing within the Europe microirrigation system market. While drip irrigation continues to dominate installed acreage, microsprinklers are rapidly gaining traction due to their wider wetting patterns, suitability for diverse soils and terrains, and flexibility across orchards, vineyards, nurseries, and plantations.

Technological advancements in pressure-compensated, clog-resistant, low-flow designs, combined with strong dealer networks and retrofit compatibility, are accelerating adoption. Growth is further supported by the expansion of high-value crop cultivation, rising climate variability, and increasing demand for versatile, multi-functional irrigation systems.

Farmers Segment to Dominate Market Demand

By end user, the farmers segment is expected to account for the largest share of the Europe microirrigation system market in 2025. Adoption is strongest among growers of orchards, vineyards, olives, fruit crops, and greenhouse horticulture, where irrigation precision directly influences yield stability, crop quality, and profitability.

Microirrigation systems have evolved into core production infrastructure, supported by strong dealer-installer-agronomic ecosystems across Europe that provide system design, financing, installation, and after-sales services. This environment accelerates system upgrades and the replacement of outdated irrigation technologies.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=222332152

Spain: Market Leader in Europe

Spain is projected to capture the largest share of the Europe microirrigation system market in 2025. High dependence on irrigation, recurring droughts, groundwater regulation, and declining reservoir levels have made efficient irrigation systems indispensable.

Spanish agriculture has adopted microirrigation as a strategic necessity for regulatory compliance, water efficiency, yield stability, and economic viability. Major demand hubs include Andalusia, Murcia, Valencia, Castilla-La Mancha, and Aragon, where drip and microsprinkler systems play a critical role in managing dry climates, saline soils, and variable rainfall.

Competitive Landscape

The market is supported by a strong global and regional supplier ecosystem. Leading Europe Microirrigation System Companies include:

- Netafim (Israel)

- Rain Bird Corporation (US)

- The Toro Company (US)

- Rivulis (Singapore)

- Valmont Industries (US)

- HUNTER INDUSTRIES (US)

- Nelson Irrigation (US)