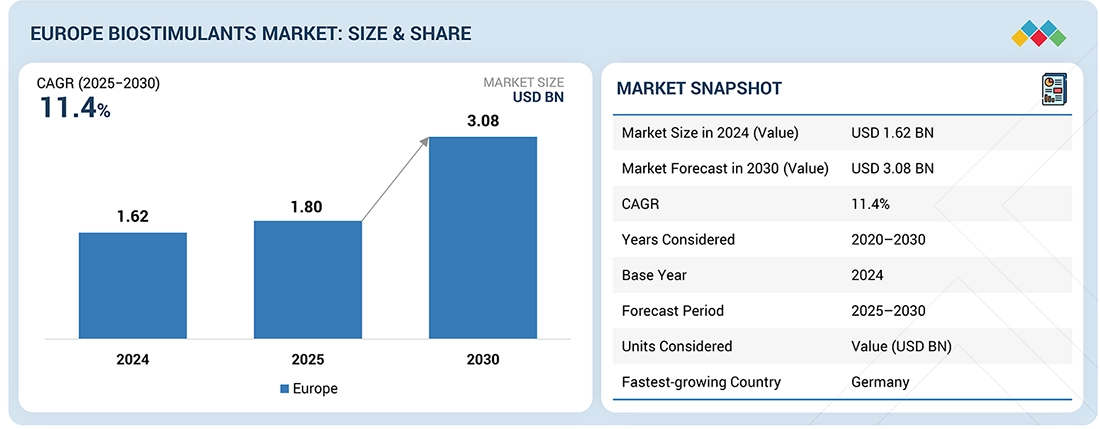

The Europe biostimulants market is on a strong growth trajectory and is projected to reach USD 3.08 billion by 2030, expanding at a CAGR of 11.4% from 2025 to 2030. This sustained expansion reflects accelerating Europe biostimulants market growth, driven by the region’s transition toward sustainable, low-input, and eco-friendly agricultural systems.

Across Europe, farmers, agribusinesses, and commercial growers are increasingly adopting biostimulants as part of integrated crop management strategies aimed at improving nutrient use efficiency, stress tolerance, yield stability, and soil health. Demand is particularly strong in key agricultural economies such as Germany, France, Italy, Spain, and the Netherlands, where biostimulants are widely applied across cereals, oilseeds, fruits, vegetables, and high-value specialty crops.

Rising awareness of climate variability, soil degradation, and sustainability goals is accelerating the use of microbial, seaweed-based, and amino-acid-based biostimulants. In parallel, the integration of digital agronomy platforms, precision agriculture technologies, and advanced distribution networks is improving product accessibility, application efficiency, and adoption rates across both large-scale commercial farms and specialized crop producers throughout Europe. These structural drivers are reshaping the Europe biostimulants industry into a core pillar of sustainable food production.

Liquid Segment Dominates the Form Category

The liquid segment holds a dominant share within the form segment of the Europe biostimulants market. This leadership is driven by its ease of application, rapid absorption, and compatibility with modern crop management systems.

Liquid biostimulants enable precise dosing through foliar sprays, fertigation systems, and seed treatments, making them suitable for a wide variety of crops, including cereals, fruits, vegetables, and specialty crops. Their formulation flexibility ensures uniform distribution, enhanced nutrient uptake, improved stress resilience, and optimized crop performance, aligning well with Europe’s push for sustainable and high-efficiency farming practices.

Ongoing innovation in stabilized and concentrated liquid formulations continues to strengthen this segment’s market dominance and commercial scalability.

Cereals & Grains: A High-Growth Crop Segment

By crop type, the cereals & grains segment is expected to grow at a significant rate in the Europe biostimulants market. This growth is supported by Europe’s extensive cultivation of wheat, barley, maize, and other staple crops, which require scalable, cost-efficient, and sustainable crop enhancement solutions.

Increasing regulatory restrictions on synthetic agrochemicals, combined with rising demand for residue-free and environmentally safe farming inputs, are pushing farmers toward biological solutions. Microbial-based and biochemical biostimulants support soil health, nutrient efficiency, pest resistance, and yield stability, making them highly attractive for cereal production systems.

The integration of precision agriculture tools and digital crop monitoring platforms is further accelerating adoption, positioning cereals and grains as a structurally important growth segment within Europe’s biostimulants ecosystem.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=16226008

UK: A Strategic Market Leader in Europe

By country, the UK holds a significant share of the Europe biostimulants market. This leadership is supported by the UK’s technologically advanced agricultural sector, strong sustainability policies, and a well-established regulatory framework for eco-friendly agricultural inputs.

UK farmers and agribusinesses are increasingly adopting microbial, seaweed-based, and amino acid biostimulants to improve nutrient efficiency, enhance tolerance to abiotic stress, and stabilize yields across cereals, horticultural crops, and high-value specialty crops.

The country’s widespread adoption of precision agriculture technologies, digital farming platforms, and smart input management systems enables optimized biostimulant application and higher return on investment. Strong distribution infrastructure, increasing soil health awareness, and government-backed sustainability initiatives further reinforce the UK’s position as a key growth hub for European biostimulant companies expanding across the region.

Leading Europe Biostimulants Companies:

The competitive landscape includes both multinational agriscience leaders and specialized biological solution providers:

- UPL Limited (India)

- Syngenta AG (Switzerland)

- BASF SE (Germany)

- Bayer AG (Germany)

- Corteva Agriscience (US)

- Biostadt India Limited (India)

- Biolchim S.p.A. (Italy)

- Koppert Biological Systems B.V. (Netherlands)

- Valagro S.p.A. (Italy)

- Isagro S.p.A. (Italy)

- Novonesis A/S (Denmark)

- Tradecorp International S.A. (Spain)

- Seipasa S.A. (Spain)

- Italpollina S.p.A. (Italy)

- Stoller Europe S.L. (Spain)