The global Erythropoietin (EPO) biomarkers market is entering a high-growth phase, projected to expand from USD 0.69 billion in 2025 to USD 1.06 billion by 2030, at a CAGR of 9.0%. This growth trajectory reflects a broader shift toward precision diagnostics, biomarker-guided therapies, and value-based care models, particularly in nephrology and oncology.

As healthcare systems increasingly prioritize early disease detection, treatment personalization, and outcome optimization, EPO biomarkers are becoming integral to clinical decision-making across multiple therapeutic domains.

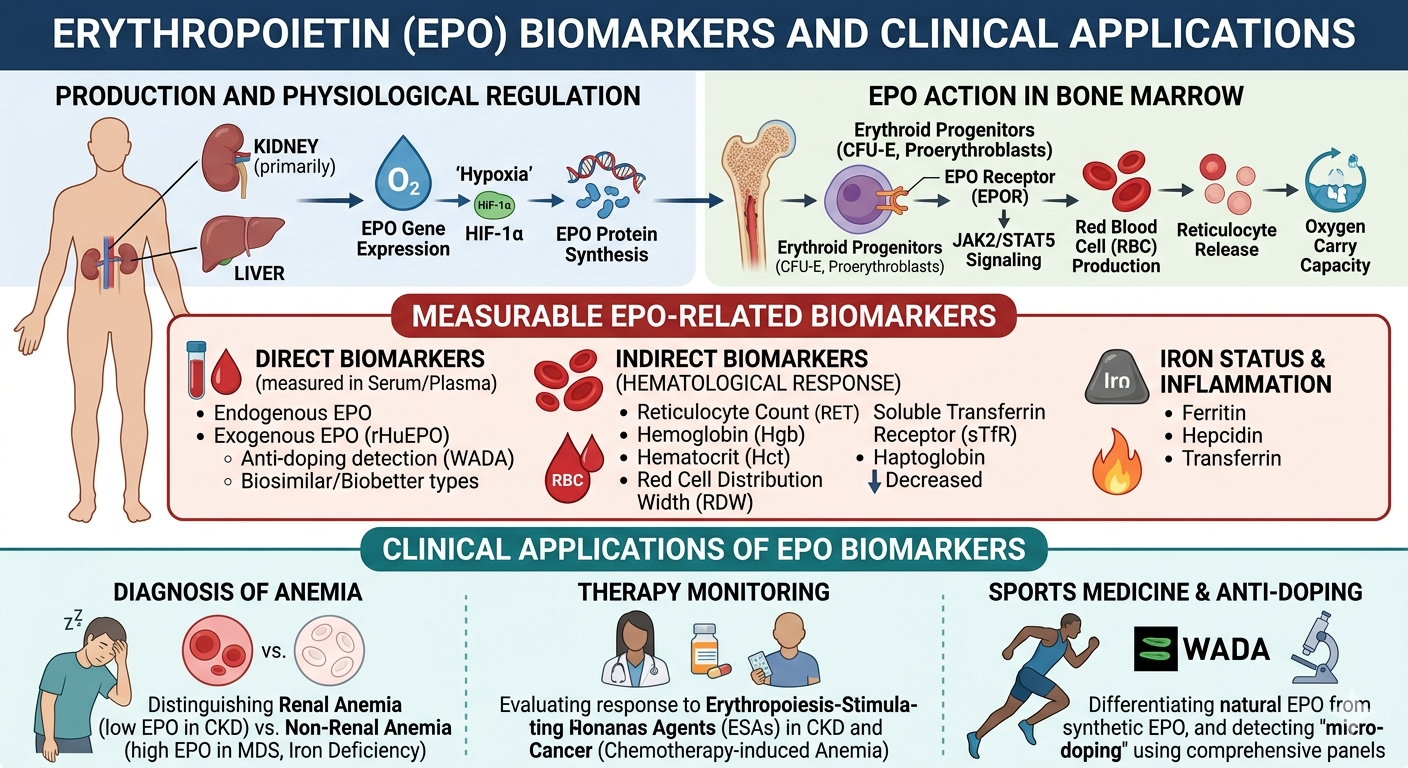

Market Dynamics: Why EPO Biomarkers Are Gaining Strategic Importance

Rising Burden of CKD and Anemia

The growing prevalence of chronic kidney disease (CKD) and anemia-related disorders is a primary demand driver. CKD patients frequently develop anemia due to impaired erythropoietin production, necessitating continuous biomarker monitoring for effective disease management.

Shift Toward Precision Medicine

Healthcare providers are increasingly adopting biomarker-based stratification to tailor therapies. EPO biomarkers enable clinicians to:

- Optimize dosing of erythropoiesis-stimulating agents (ESAs)

- Reduce risks associated with over- or under-treatment

- Improve patient outcomes through real-time monitoring

Download PDF brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=246612734

Technological Advancements in Diagnostics

Innovations in immunoassays, multiplex platforms, and automated analyzers are enhancing the sensitivity, throughput, and scalability of EPO testing. These advancements are making biomarker testing more accessible across both centralized and decentralized healthcare settings.

Segment Insights

Hospitals Lead the End-User Segment

Hospitals accounted for the largest share of the EPO biomarkers market in 2024—and for good reason.

They operate high-throughput diagnostic laboratories equipped with centralized immunoassay systems capable of handling large patient volumes. Hospitals also manage complex cases involving CKD and oncology, where multi-parameter diagnostics (EPO, reticulocytes, ferritin) are essential.

Key advantages include:

- Integrated clinical workflows for anemia management

- Skilled laboratory personnel and advanced infrastructure

- Established reimbursement frameworks

- Faster turnaround times for critical diagnostics

This makes hospitals the primary hub for EPO-based diagnostic and therapeutic decision-making.

Cancer Segment: Fastest-Growing Application Area

The oncology segment is expected to register the fastest growth during the forecast period.

Chemotherapy-induced anemia is a common complication in cancer patients, creating strong demand for real-time biomarker monitoring. EPO biomarkers are increasingly used alongside other hematologic indicators to guide ESA therapy.

Growth drivers include:

- Rising incidence of cancer globally

- Increased adoption of multiplex immunoassays

- Expansion of biomarker-driven clinical trials

- Growing use of biosimilars in oncology care

In both hematological malignancies and solid tumors, EPO biomarkers are becoming essential for precision dosing and therapy optimization.

Regional Landscape: North America at the Forefront

North America dominated the global EPO biomarkers market in 2024, supported by a mature healthcare ecosystem and strong innovation pipeline.

Key factors behind its leadership:

- Presence of advanced academic medical centers and integrated health systems

- Rapid adoption of automated and multiplex diagnostic technologies

- Favorable reimbursement policies for anemia monitoring

- Early regulatory acceptance of novel diagnostic platforms

- Strong investment in clinical trials and real-world evidence generation

Additionally, ongoing initiatives in precision nephrology and oncology continue to reinforce the region’s dominant position.

Competitive Landscape: Key Industry Players

The EPO biomarkers market is moderately consolidated, with major pharmaceutical and diagnostics companies driving innovation and commercialization. Leading players include:

- Amgen Inc.

- Biocon Ltd.

- Johnson & Johnson

- F. Hoffmann-La Roche Ltd

- Merck KGaA

- Pfizer Inc.

- Siemens Healthineers

- 3SBio Group

These companies are actively engaged in:

- Expanding biomarker assay portfolios

- Developing biosimilar EPO therapies

- Investing in companion diagnostics

- Strengthening global distribution networks

Strategic Outlook: Where the Market Is Heading

The EPO biomarkers market is poised for sustained expansion, underpinned by several macro and micro trends:

- Integration of AI and data analytics into biomarker interpretation

- Growth of decentralized and point-of-care testing models

- Increasing focus on value-based healthcare delivery

- Expansion of biosimilars and cost-effective treatment pathways

- Rising demand in emerging markets, particularly in Asia-Pacific

For stakeholders—including diagnostics companies, pharma players, and healthcare providers—the opportunity lies in aligning biomarker innovation with clinical utility and economic value.

Conclusion

Erythropoietin biomarkers are transitioning from niche diagnostic tools to core components of precision medicine frameworks. With strong growth fundamentals, expanding clinical applications, and continuous technological innovation, the market is well-positioned to reach USD 1.06 billion by 2030.

Organizations that invest in advanced diagnostics, integrated care pathways, and biomarker-driven insights will be best positioned to capture value in this evolving landscape.